Fishing for Fed’s Independence

David R. Kotok, December 22, 2024

(The following was first published on The Kotok Report website and via LISTSERV. For details, visit https://kotokreport.com/.)

First, I want to wish all readers the very best and safest holiday celebrations. Our Congress celebrated, too, by giving the United States an added cost of about $50 billion a year in the nation’s interest rate burden. I will offer evidence of this assertion below; note, the one-year tenor CDS rose 2 basis points on the CR fiasco. The 5 and 10 yr. are already elevated. I totally agree with President-elect Trump. The debt ceiling nonsense should stop, and the entire country would benefit. The proof and the cost are depicted below.

Now let me turn the clock back to Labor Day weekend in 2019: The Fed’s balance sheet had been shrinking for a few months; No Covid-19 shock; federal deficits appeared manageable with primary deficits heading for surplus. Halcyon days. You will find that date in the bottom set of charts.

In his recent paper for the Hoover Institution, former Philly Fed president Charles Plosser opened with this paragraph:

The debate over the appropriate relationship between monetary policy and fiscal policy is an old one. However, it has taken on renewed significance since the crisis of 2007-2008 as both the Fed and the Treasury have initiated policies that breached accepted norms that had largely been in place since the Treasury-Fed Accord of 1951. My view is that these actions have undermined the institutional arrangements intended to support the independence of our central bank and frayed the boundaries between monetary and fiscal policies.

You can find the entire paper here: “Crumbling Boundaries and the Risks to Central Bank Independence,” https://www.hoover.org/sites/default/files/research/docs/24115-Plosser.pdf

Charlie Plosser’s paper offered some American history. Here’s an excerpt:

The political failures of the early attempts to establish a central bank in the U.S. were so distasteful that it took nearly three-quarters of a century after the closing of the Second Bank of the United States before the Congress created the Federal Reserve System in 1913. It was designed as a decentralized institution with a geographical dispersion of semi-private Reserve Banks and a Board of Governors in Washington. Part of the motivation was to support a more decentralize decision-making process, with a diversity of views with less focused on the financial centers and the short-run politics in Washington.

After the collapse of the gold standard, changes were made in the Fed’s governance structure. The Banking Act of 1935 removed the Treasury Secretary and the Comptroller of the Currency from the Fed’s governing board, granted governing board members 14 year terms and established a new legal entity, the Federal Open Market Committee (FOMC), to govern the conduct of open market operations (the purchase and sale of government securities). These changes reduced the fiscal authority’s direct participation in the governing board, but granted greater authority to the political appointed Board of Governors in open market decisions relative to the Reserve Bank presidents. These changes are evidence of the struggle to establish boundaries between monetary and fiscal policy.

The Treasury-Fed Accord of 1951 was an important milestone in support of Fed independence. It was an agreement between the Fed and the Treasury that the central bank would control its own balance sheet rather than tailoring its purchases and sales of government securities at the behest of the Treasury.

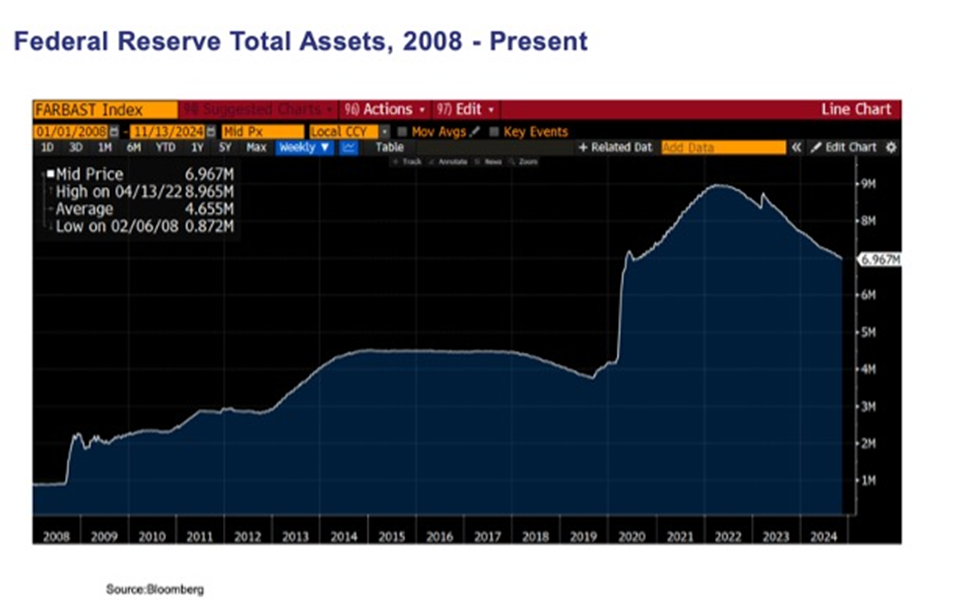

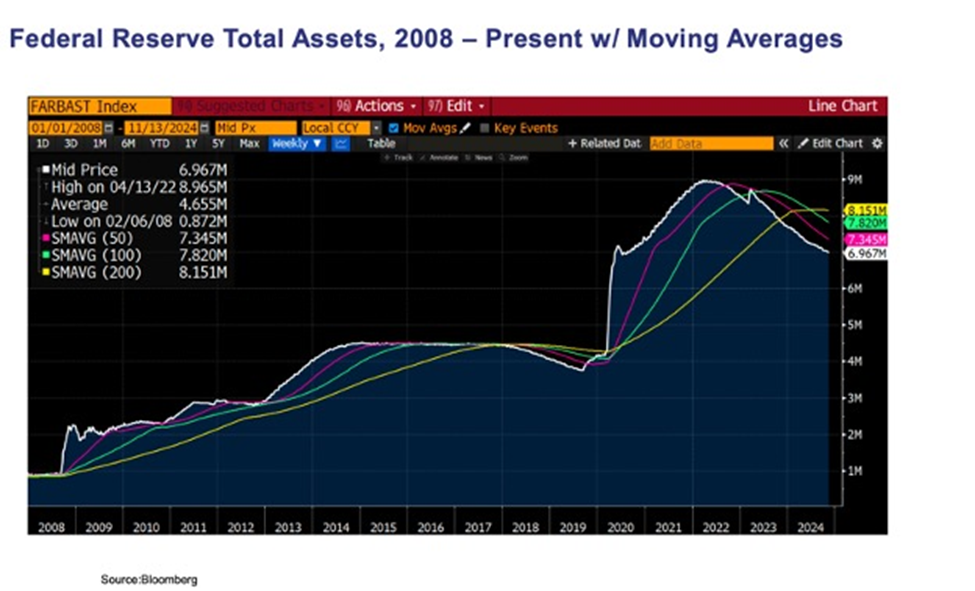

The following chart was inserted to show the growth of the Fed’s balance sheet since its 2008 as a response to the Great Financial Crisis and subsequently the additional enlargement in response to the Covid pandemic shock. Some moving-average smoothing was used to make the second chart easier on the eyes. This chart is Bloomberg data; the second one is Bloomberg showing the various moving averages.

{kind=link}

{kind=link}

There is a need for central bank independence. But what happens when the fiscal authority becomes the culprit? In other words, when the government runs continual and increasing deficits and fails miserably in its fiscal function.

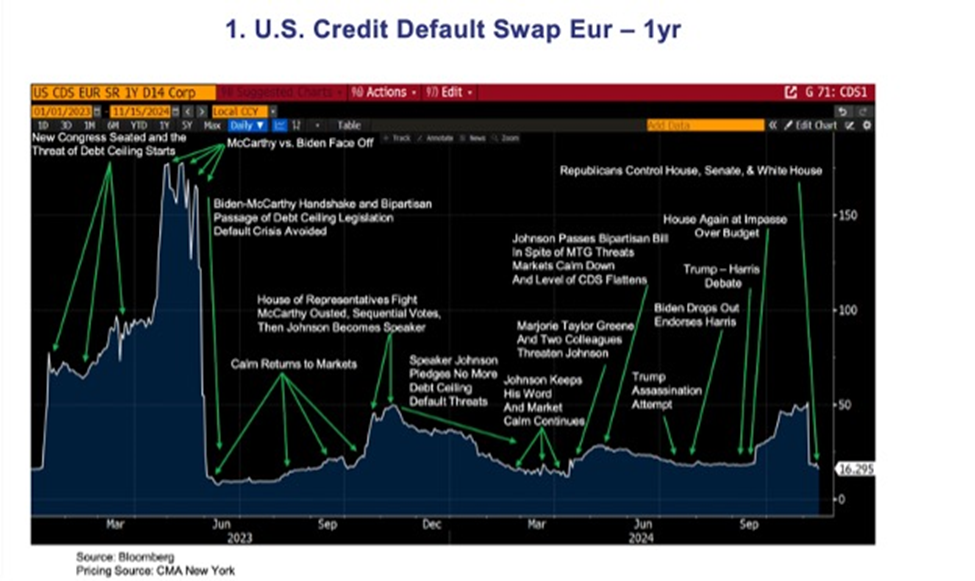

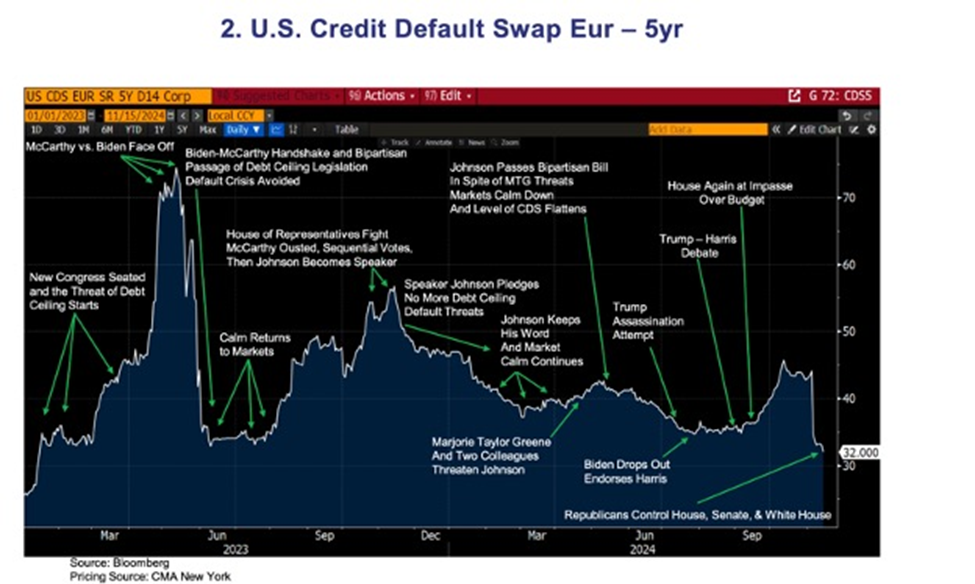

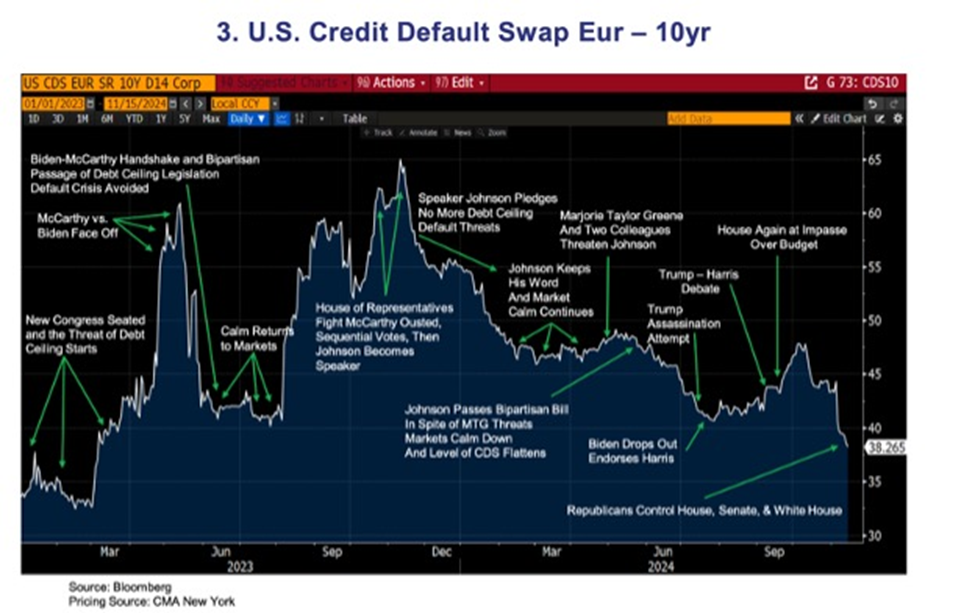

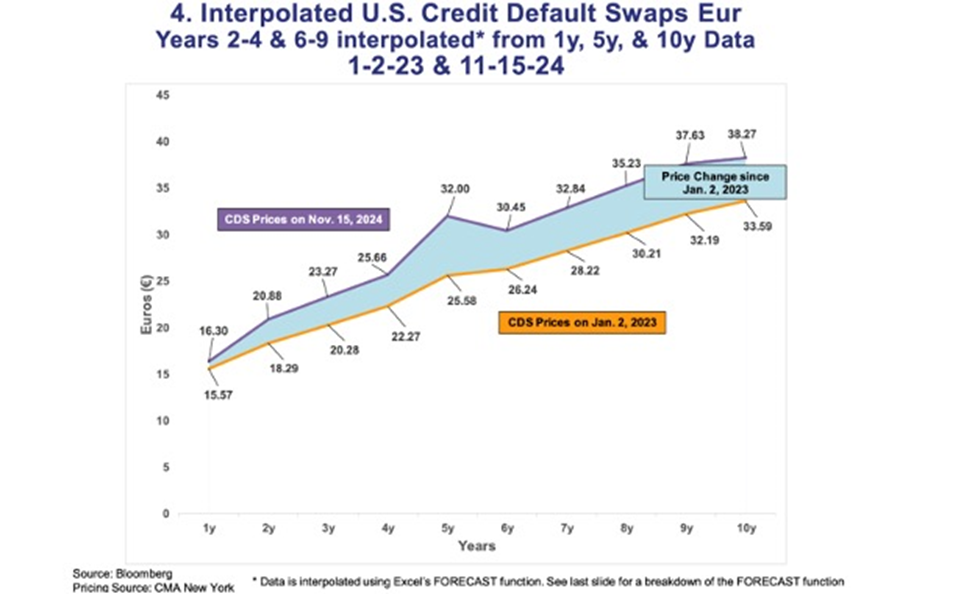

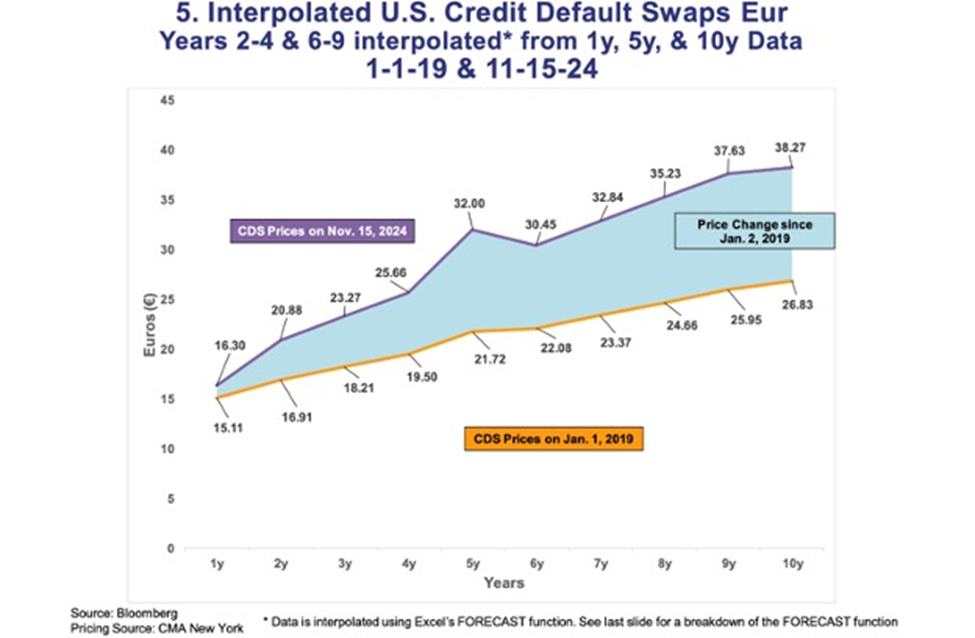

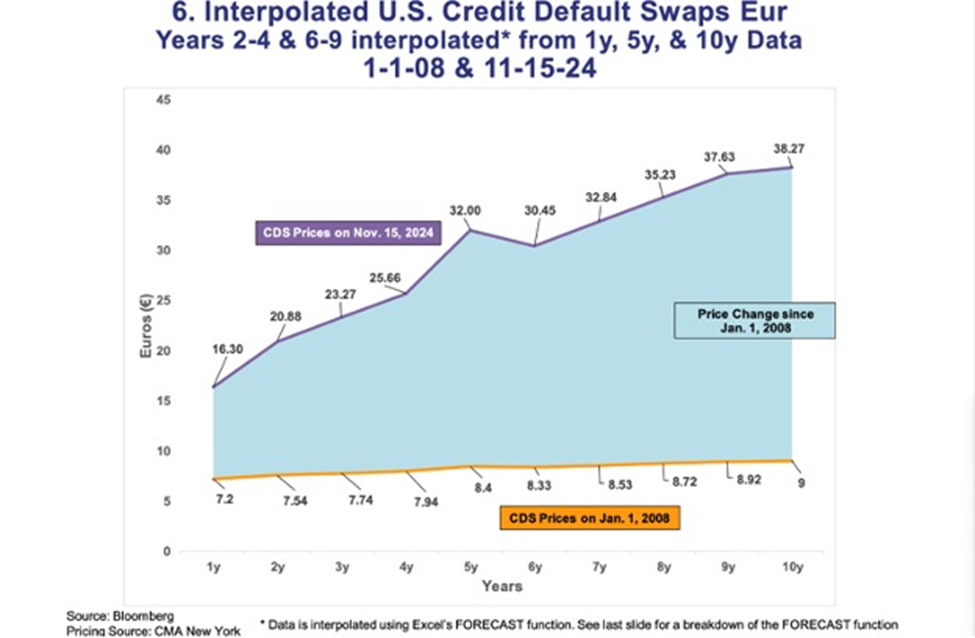

The following charts show the pricing of the creditworthiness of the United States as seen through the eyes of foreigners. And they show the trends since 2008 when the Fed first initiated its balance sheet expansion. These six charts tell the story of American politics. The first three are of different time periods: Chart 1, the last two years; Chart 2, the period since before Covid; and Chart 3, the entire period from 2008. All the periods and CDS pricing and political events are marked. The second three charts (numbers 4-5-6) compare the entire curve of CDS for the same time periods and what happened from the start to the end of each period.

Here are the six charts. It may take a reader some time to digest the data. Pls. look at the notes and details.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Chart 6 shows where America’s creditworthiness was priced in 2008 and where it was priced after our election results were finally known in mid-November 2024. Please note the light blue shaded area that depicts the comparison. That is where pricing of America’s creditworthiness was in 2008 and where it is now.

Conclusions: the cost of insuring the creditworthiness of the United States went up in each period.

When you consider that the price of America’s creditworthiness has changed and is higher than it was in 2008, one must ask how this change is reflected in market actions.

So, we will pose a question to readers:

Since the Fed can set any interest rate anywhere it wants and keep it there, is it the size of the balance sheet of the Fed that is now the “shock absorber” for the deteriorating pricing of US creditworthiness? In other words, does the Plosser warning about the “fiscal authority” apply now? And if it does, doesn’t that mean we must fiercely defend the independence of the central bank from an attack by the fiscal authority?

On Thursday afternoon, I wrote this in a note sent to some colleagues. “1-year tenor CDS rose 2 basis points today. 5 and 10 yr. were already elevated in the high 30s. On $28 trillion of tradeable UST debt (exclude what the gov’t owes itself) each basis point means $28 billion of added financing pressure on the US. Since the Fed ignores this and manages the interest rate. The pressure is revealed in the necessity to have a larger and larger balance sheet at the central bank. My guesstimate is that the Fed should cease QT now. Or very soon. They are getting close. And the repo cushion that helped in the last shock is gone. Congressional miscreants are playing with very large matches. Happy Christmas, Chanukah, Kwanzaa. “The country’s in the Very Best of Hands.” Li’l Abner